At the Spring Statement 2022, the Chancellor announced measures related to National Insurance contributions (NICs) and income tax.

This factsheet provides an overview of the announcements.

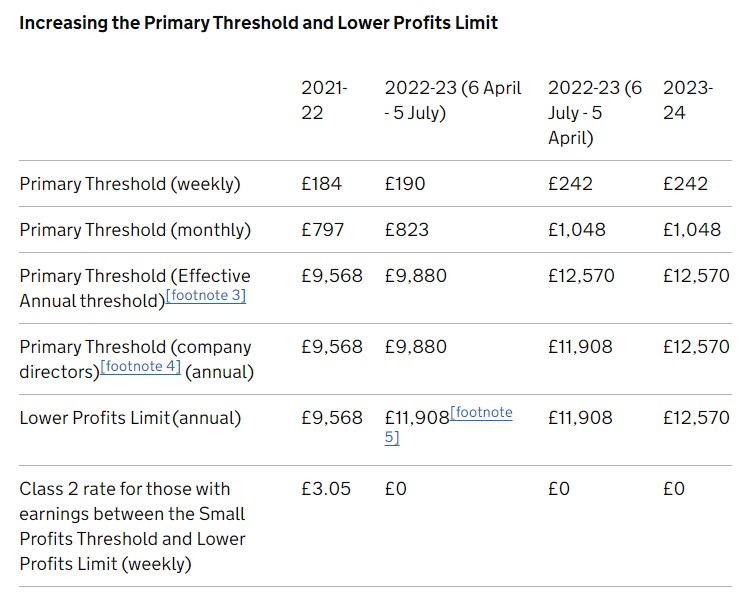

- We are raising the level at which people start to pay National Insurance contributions, increasing the National Insurance Primary Threshold (PT) and Lower Profits Limit (LPL) from £9,880 to £12,570. Further details on implementation are set out in the background section of this factsheet.

- This is a tax cut worth over £330 for a typical employee in the year from July 2022.

- We are also cutting income tax. Taxpayers will gain £175 on average thanks to a 1ppt cut in the basic rate of income tax in 2024, the first cut to the basic rate in 16 years.

We are helping hard-working families with the cost of living

- We will increase the Primary Threshold and Lower Profits Limit – the point at which employees and the self-employed start paying National Insurance contributions (NICs) – to bring them in line with the income tax personal allowance of £12,570.

- This will mean working people will be able to earn £12,570 tax free, an increase of £2,690 in cash terms.

- This will benefit almost 30m working people. This is a tax cut for a typical employee worth over £330[footnote 1] in the year from July 2022; the equivalent saving for a typical self-employed person would be worth over £250.

- To ensure all individuals see the benefits of the increase as early as possible, while also allowing employers and payroll software providers sufficient time to update their systems, the increase will be implemented from July 2022.

We are supporting the lowest earners to keep more of the money they earn

- From July, around 70% of workers who pay NICs will pay less NICs than they otherwise would have, even after accounting for the introduction of the Health and Social Care Levy.

- Due to this measure, 2.2 million people will be taken out of paying Class 1 (Employee NICs) and Class 4 NICs (Self-employed NICs) and the Health and Social Care Levy entirely, on top of the 6.1 million workers who already do not pay NICs.

- We are also reducing Class 2 NICs payments for lower earning self-employed individuals. From April 2022 self-employed individuals will not pay Class 2 NICs on profits between the Small Profits Threshold (£6,725) and Lower Profits Limit, but they will continue to be able to build up National Insurance credits. This will benefit around half a million self-employed people by up to £165 a year.

- Taken together, these measures will meet the government’s ambition to ensure that the first £12,500 earned is tax free.[footnote 2]

Income tax

- The government will cut the basic rate of income tax by 1ppt from April 2024.

- This is the first cut to the basic rate of income tax in 16 years (the last cut to the basic rate was in 2008-09).

- Over 30m taxpayers will benefit from this policy in 2024-25, with an average gain of £175.

- There will be a three-year transition period for Gift Aid relief to maintain the income tax basic rate relief at 20% until April 2027. This will support almost 70,000 charities and is worth over £300m.

- The cut will apply to the basic rate which applies to non-savings, non-dividend income for taxpayers in England, Wales and Northern Ireland; the savings basic rate which applies to savings income for taxpayers across the UK; and the default basic rate which applies to a very limited category of income taxpayers made up primarily of trustees and non-residents.

- It is fully costed and fully paid for, including additional funding for the Scottish Government as this is a devolved matter in Scotland.

Background: What does a July implementation mean for employees and the self-employed?

What this means for employees

- Between 6 April and 5 July 2022, employees will be able to earn £190 a week without paying Class 1 NICs and the Levy.

- Between 6 July 2022 and 5 April 2023, this weekly threshold will increase to £242.

- From April 2023 onwards, employees will be able to earn £242 each week, equivalent to £12,570 a year, without paying Class 1 NICs or the Levy.

- The PT will then remain aligned with the income tax personal allowance.

- Employees entitlement to contributory benefits are unaffected by this measure. What this means for the self-employed

- The self-employed pay NICs on an annual basis, and at the end of the tax year. For the 2022-23 tax year, the self-employed will be able to earn £11,908 before paying Class 4 NICs and the Levy. The annual figure for the self-employed is £11,908, because this accounts for 13 weeks of £9,880 and 39 weeks of £12,570. That means the benefit the self-employed receive in 2022-23 is in line with employees.

- From April 2023 onwards, the self-employed will be able to earn £12,570 before paying any NICs.

- The LPL will then remain aligned with the income tax personal allowance.

- Further, for 2022-23, the point at which the self-employed start paying Class 2 NICs will increase to £11,908. This means that those with profits between the Small Profits Threshold (£6,725) and the LPL (£11,908) will not need to pay Class 2 NICs from April 2022, but will still be able to access entitlement to contributory benefits.

Footnotes:

- The tax cut is worth £332 to all employees who have only one job and who earn above the Primary Threshold in each pay period across the year from July 2022. The equivalent figure for a self-employed individual is reached by adjusting the employee savings figure to reflect the lower rates of Class 4 NICs paid by the self-employed.

- There may be some individuals who continue to pay NICs even if annually they earn less than £12,570, for example, someone whose earning all fall in a single week or month. This is because NICs is charged on a pay period basis and is not annualised, cumulative or aggregated.

- “Effective Annual threshold” refers to the Primary Threshold level if the weekly level was applied for a full year.

- This is the threshold for people who are subject to company director rules. The annual equivalent for the period 6 July 2022 to 5 April 2022 is £11,908 because this accounts for 13 weeks of £9,880 and 39 weeks of £12,570.

- The self-employed pay NICs on an annual basis, and at the end of the tax year. The annual figure for the self-employed is £11,908 because this accounts for 13 weeks of £9,880 and 39 weeks of £12,570.